The EU Carbon market prices - historical and future outlook

The EU carbon market

The EU carbon market consists of carbon allowances that energy-intensive sectors need to buy to compensate for their greenhouse gas (GHG) emissions. This market is known as The EU Emissions Trading System (EU ETS). Currently, the economic actors mandatory for participating in this trading system are the power, industry, aviation, and from 2024 the maritime sectors. One European Emission Allowance (EUA) gives the holder the right to emit 1 tonne of CO2 and is quoted in EUR, effectively putting a price on the emission of 1 tonne of CO2.

Historical prices - timeline

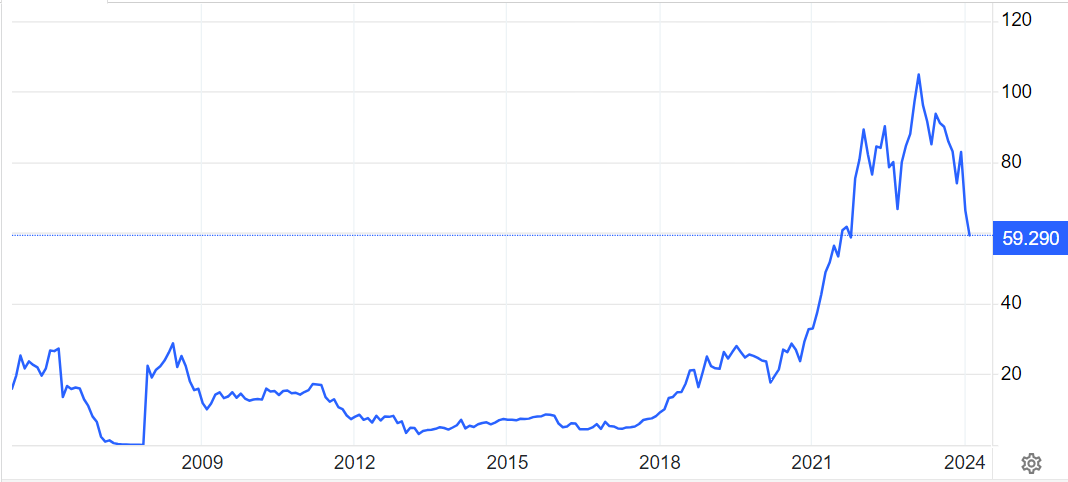

The graph shows the historical prices of an EUA since its launch in 2005. Uncertainties and a generous free allocation of allowances led to a slow start with prices hovering around 5-25 EUR/t. A trading collapse in 2006 saw prices drop to near zero due to excess allowances. The prices then stabilized below 20 EUR/t, before a gradual incline began in 2018. Significant market reforms introduced in 2019 and 2021, including reducing free allowances and introducing a market stability reserve, tightened the supply and led to a dramatic price increase.

In February of 2023, it reached an all-time high of 105.73 EUR/t. From that point, it has been a rather steep decline. So far, in February of 2024, the prices have been ranging in the mid-high 60s to higher 50s - where it is today at 59.290 EUR/t.

The recent dip in prices from 2023 to 2024 can be explained by mild winter, falling natural gas prices, and high gas inventories. Europe’s unusually warm winter has dampened energy demand, reducing the need for carbon allowances. Furthermore, European natural gas prices remain low due to persistently low demand and healthy gas reserves. Cheaper gas, a key fuel for power generation, reduces energy producers’ reliance on carbon-intensive coal, thus lowering demand for EUAs.

Key price drivers for the coming months: Bearish

Predicting future prices is notoriously difficult, however, we can see a couple of key drivers for EUAs going forward. Politically, 2024 is coined the mega election year with major elections happening all over the world. The EU is set to elect a new parliament and a new executive commission come June. The EU’s Fit for 55 policy is also expected to be a tightening factor in the coming months. However, the mild weather temperatures throughout Europe, the decreasing gas prices, and the relatively high gas inventory levels currently at 66 % (AGSI, 2024) also contribute to short-term price suppression. Nordic hydrobalance is also stable and weather forecasts for the Nordic countries are also expected to be mild in the coming weeks. The ongoing El Niño can also be a contributing factor to a wetter and warmer Europe this spring which can contribute to further downward pressure in the coming months.

In conclusion, we see the general short-term outlook as bearish with some possible negative externalities like the uncertain political outcomes both in the U.S. primary elections in August and in Europe this June, as well as the new sector (maritime) that needs to conform to the new trading system (which means an additional supply of EUAs). Weather outlooks going ahead are impossible to predict, but an expected wetter and hotter Europe than usual might suppress prices further..

.PNG)

Kommentarer

Legg inn en kommentar